Learn how to check and verify if a money order is fake, whether it was issued from a bank or the USPS, and see the signs that it may be part of a scam.

Money orders can be a great way to exchange funds if you prefer a non-electronic option but don’t have access to paper checks from a bank account. Although there’s a level of convenience associated with this payment type, but you still have to check if the money order is a possible fake. Trying to deposit or cash a fake money order, could cost you money in the end. Your bank could hold you responsible for those funds or any other fees assessed with returned payments or insufficient funds. For this reason, it’s worth taking a moment to learn about spotting fake money orders. There are several ways to tell if a money order is fake or not.

There are different kinds of money orders that come from different places like banks or other financial institutions. We’ll go over a few common money order types and how to spot fake ones. But here are some general tips on how to check any kind of money order:

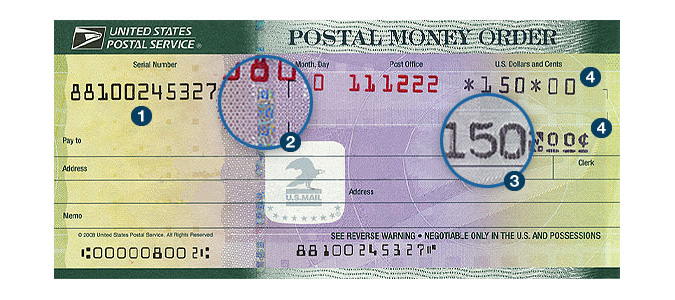

According to the USPS website, here are ways you can check the authenticity of one of their money orders:

The USPS provides a way to verify money orders. If you’re not sure if the money order is real or not, you can call the U.S. Postal Service Money Order Verification System at 866-459-7822.

You can also report any suspected fraud by calling the U.S. Postal Inspection Service at 1-877-876-2455.

When you get a money order from a financial institution, there will often be information, right on the money order, concerning watermarks, how the money order should look on the back and other security features.

If you don’t see any of this information, that is a huge red flag and could mean that a money order is fake.

Photocopied money orders may also show obvious markings like “void” or “copy” on them. These words are designed to show up when someone attempts to make a photocopy. If you see these markings, then your money order is fake.

Other clues include dollar amounts over $1,000, smudged ink or flimsy paper stock. If you hold the money order up to the light and don’t see watermarks or faint designs, your bank-issued money order may not be authentic either.

The optimal verification step would be to bring the suspect money order with you to the bank that issued it.

This way, you can hear from the source whether or not the money order is legitimate with the right funds behind it.

You can cash it right away (be prepared to provide the necessary documentation to verify your identity).

Just like any other money order, you will look for security features such as watermarks that should be visible when held to the light, legal amounts, etc.

For instance, Money Gram money orders have a heat-sensitive mark that fades and reappears when you touch it with your thumb or finger.

Both Western Union and Money Gram money orders also have a receipt you can tear off for your records. If they are real, these money orders should have perforated edges on one side.

You can also verify the authenticity of these money orders by calling their verification hotline:

If you deposit a fake money order, there’s a chance that the bank will cash it and make the funds available right away. In some cases, the bank may hold back a portion of the funds until the money order is verified.

In either case, if you spend any of the money and the money order is found to be fake, the bank will likely charge a "deposit item returned fee."

Here’s what you can expect to pay at different banks for return deposit fees:

| Bank | Domestic Returned Deposit Fee | Foreign Returned Deposit Fee |

|---|---|---|

| Chase | $12 | $12 |

| Bank of America | $12 | $15 |

| Wells Fargo | $12 | $15 |

| Citibank | $12 | $12 |

| U.S. Bank | $19 | $25 |

| Truist | $12 | $30 |

| PNC Bank | $12 | $12 |

| TD Bank | $15 | $15 |

| Capital One | $10 | $10 |

| Fifth Third Bank | $15 | $15 |

| AVERAGE | $13.10 | $16.10 |

If you are dealing with someone you don’t know, you are more likely to be a victim of financial fraud. If someone can remain anonymous, it’s much easier for them to trick you out of funds using money order scams.

When dealing with people you don’t know, accept digital payments or be prepared to verify your money order on the spot.

Carter Seuthe, founder at Credit Summit, a personal finance blog, describes how this works, “There is a common scam often referred to as the ‘overpayment ploy.’ The scammer will send a money order for a higher amount than necessary for the purchase, and then they will ask you to refund them the extra.”

Of course, the money order is bogus, but you will have cashed it and the bank will expect you to cover all the funds once they inspect it and determine that it’s fake.

Part of the money order scams can include a remitter who seems in a hurry to wrap up your deal using a fake money order. They'll urge and rush you to get to the bank and make the deposit, they can get out of the picture before the bank finds the money order fraudulent.

They may make up a story about having to leave the country, tend to a sick relative or some other sob story to make you let your guard down. Once you believe this story, you might be more likely to compromise your good sense and do business in a way that you would not normally.

Although these can be faked, too, they are another alternative payment you can accept—especially when doing business with higher dollar amounts.

Even with a cashier’s check, you still want to check watermarks, ink, paper stock, etc.

This payment method can be expensive for both the sender and recipient. Also, it’s not always as instant as other electronic forms of payment, but it still pretty quick.

However, it’s a payment method that is also almost impossible to fake. Before a bank will even approves the transfer, the funds must available in the sender’s account.

Zelle is a digital payment platform that allows you to, in most cases, send and receive verified funds instantly (limits do apply). Because of this, it’s an extremely secure, reliable means of payment.

These digital payments are also usually instant and secure. One tip when dealing with these forms of payment: When someone sends funds, just make sure they actually arrive in your account.

Don’t just go by phone or email notifications once the sender transmits the funds. You should also know that with some types of PayPal payments reversal is possible.

So, make sure whoever is paying you is reliable and unlikely to file a claim for payment reversal without cause.

It’s easier for scammers to use money orders fraudulently for a few reasons. For one, graphics on paper can be re-created with simple apps and printing equipment.

Nowadays, you don’t even need sophisticated technology to recreate a money order. Although most equipment can’t duplicate all the markings of a money order, it’s often good enough to fool some people at first glance.

Another reason money orders are easy targets for scammers is the fact that there is a process to convert them into cash. Once you walk away with a money order, there are additional steps that take time to complete, as opposed to a digital transaction that takes place in a few moments with verified funds.

By the time you reach the bank with a fraudulent money order, it’s almost too late. Even the cashier at the bank may cash your money order without doing a check for authenticity. Once it’s cashed, the bank could hold you liable for the funds they cannot recoup from the fake money order.

Finally, some money order scams appeal to people’s desire to get something for nothing. As the old adage goes, if it sounds too good to be true, it probably is!

Aja is a writer and blogger based in Chicago who covers topics on personal finance and entrepreneurship. She writes from her experiences with money management and paying off $120,000 in debt. Aja has been quoted and/or featured on sites such as Time Money, Kiplinger's, U.S. News & World Report, Market Watch, and more. Education: B.A. in University of Illinois Urbana-Champaign.

We believe by providing tools and education we can help people optimize their finances to regain control of their future. While our articles may include or feature select companies, vendors, and products, our approach to compiling such is equitable and unbiased. The content that we create is free and independently-sourced, devoid of any paid-for promotion.

This content is not provided or commissioned by the bank advertiser. Opinions expressed here are author’s alone, not those of the bank advertiser, and have not been reviewed, approved or otherwise endorsed by the bank advertiser. This site may be compensated through the bank advertiser Affiliate Program.

MyBankTracker generates revenue through our relationships with our partners and affiliates. We may mention or include reviews of their products, at times, but it does not affect our recommendations, which are completely based on the research and work of our editorial team. We are not contractually obligated in any way to offer positive or recommendatory reviews of their services. View our list of partners.

MyBankTracker has partnered with CardRatings for our coverage of credit card products. MyBankTracker and CardRatings may receive a commission from card issuers. Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.