- For loans with a maturity that exceeds 12 months:

- Loans of $1,000,000 or less: 0.00%.

- Loans of $1,000,001 to $2,000,000: 1.45% of the guaranteed portion of the loan up to and including $1,000,000, plus 1.70% of the guaranteed portion of the loan over $1,000,000.

- Loans of $2,000,001 and greater: 3.50% of the guaranteed portion of the loan up to and including $1,000,000, plus 3.75% of the guaranteed portion of the loan over $1,000,000.

- Loans of $1,000,000 or less: 0.00%.

- Loans $1,000,001 and greater: 0.25% of the guaranteed portion.

In most deals with SMB investors, the guarantee and closing costs will be rolled into total uses of the deal, meaning the buyer will get credit for paying these as a form of equity.

Payment Terms

- Repayment terms: As a buyer, SBA financing will more than likely be used for the purchase of business; therefore, the repayment term a buyer will typically see is 10 years. Depending on the purpose of the SBA 7(a) loan, the repayment term could be as long as 25 years. It’s common for business acquisitions including real estate to include a longer term.

- Prepayment: If an SBA 7(a) loan has a maturity less than 15 years, then the buyer does not have to worry about a prepayment penalty. However, if the loan matures in 15 or more years, there is a prepayment penalty if the borrower pays more than 25 percent or more of the outstanding loan balance. The prepayment penalty is only applicable for the first 3 years of the loan. The size of the prepayment penalty is dependent on when the prepayment occurs. The prepayment penalty ranges from 5 percent to 1 percent of the amount that was prepaid.

- Earnest money / packaging fee: The packaging fee is paid to the lender because the lender gathers all the loan documents and makes sure the borrower (buyer) has the best chance of loan approval. Earnest money is common with SBA term sheets because it is a financial incentive for the buyer to use that lender when buying the target firm. After all, the lender put in quite a bit of time for the buyer to get the approved SBA term sheet.

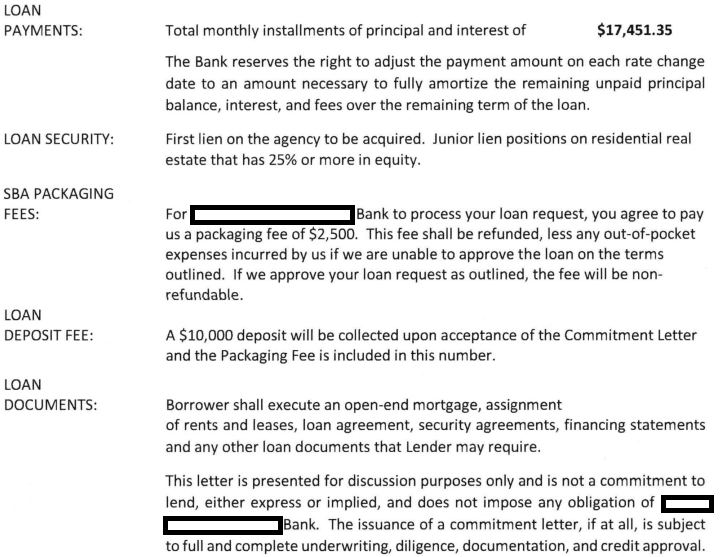

Below is an example of the applicable fees in a SBA Term Sheet:

What Comes After a Term Sheet?

Once a term sheet has been signed by the buyer of a business, the bank will begin underwriting the transaction. This involves increasing levels of diligence and will ultimately end in a commitment letter from the bank to fund the loan.

Information posted on this page is not intended to be, and should not be construed as tax, legal, investment or accounting advice. You should consult your own tax, legal, investment and accounting advisors before engaging in any transaction.

Get the latest in your inbox

Join our bi-weekly SMB newsletter. It's free and not annoying.

© 2024 Mainshares, LLC. All rights reserved. Disclosure:This website (the “Website”) is owned and operated by Mainshares, LLC (“Mainshares”). By accessing the Website and any pages thereof, you agree to be bound by Mainshares’ Terms of Service and Privacy Policy, as well as the Terms of Service and Privacy Policy for Main Street Securities, LLC (“Main Street”). The information contained herein is provided for informational purposes only and is not intended to influence any investment decision or be a recommendation for any investment, service, product, or other advice of any kind, and shall not constitute or imply an offer of any kind. The products and services offered by Mainshares are not offered by a certified public accountant (“CPA”) and should not be considered as a substitute for services provided by a CPA.

The information contained herein is provided by Mainshares, LLC (“Mainshares”) for informational purposes only and is not intended to influence any investment decision or be a recommendation for any investment, service, product, or other advice of any kind, and shall not constitute or imply an offer of any kind. The products and services offered by Mainshares are not offered by a certified public accountant (“CPA”) and should not be considered as a substitute for services provided by a CPA.

Broker-dealer services provided in connection with some of the investment opportunities on the Mainshares platform are offered through Main Street, a registered broker-dealer, affiliate of Mainshares, and member of FINRA/SIPC. For additional information, please contact your licensed securities representative of Main Street Securities LLC or visit FINRA’s BrokerCheck. If the investment opportunity does not include the "Brokered by Main Street Securities" designation, broker-dealer services were not provided in connection with the offering through Main Street.

Neither Mainshares nor Main Street Securities LLC make investment recommendations and no communication, through this Website or in any other medium should be construed as a recommendation for any security offered.

Should you be presented with an investment opportunity, such investment opportunities involve private, unregistered securities that are speculative and involve substantial risk. These investment opportunities are conducted in accordance with an exemption from registration, specifically relying on the private offering provision outlined in Section 4(a)(2) of the Securities Act of 1933, along with compliance with Rule 506 of Regulation D. All investments involve risk and the past performance of a security, or financial product does not guarantee future results or returns. There is always potential to lose money when you invest in securities or other financial products. Private placements lack liquidity and distributions are not guaranteed. You are strongly encouraged to seek professional advice prior to entering into any transaction for any securities and to consider your investment objectives and risks carefully before investing.

Neither the SEC nor any federal or state securities commission or regulatory authority has recommended or approved any investment or the accuracy or completeness of any of the information or materials provided herein or through any references/links herein. There can be no assurance that any valuations provided by issuers are accurate or in agreement with market or industry valuations. Neither Mainshares nor Main Street Securities LLC make any representations or warranties as to the accuracy of such information.